Stochastic Modeling and Simulation of Asset Prices: A Comparative Analysis of Brownian Motion, Geometric Brownian Motion, and a Jump-Diffusion Model

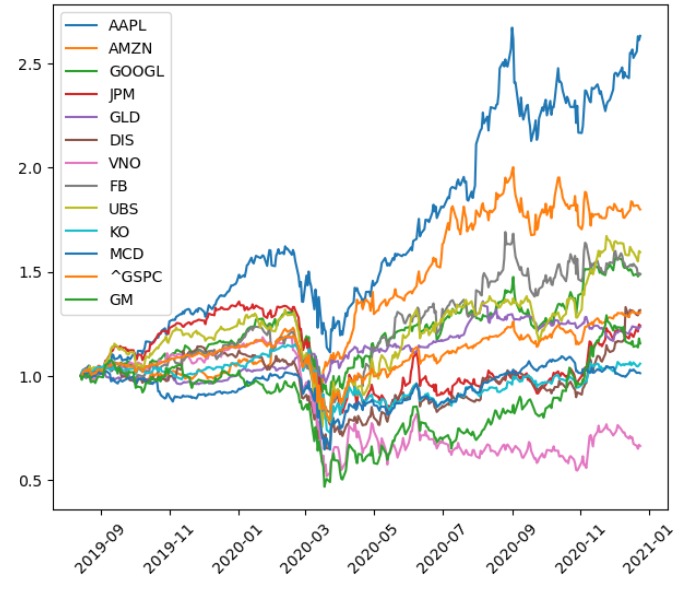

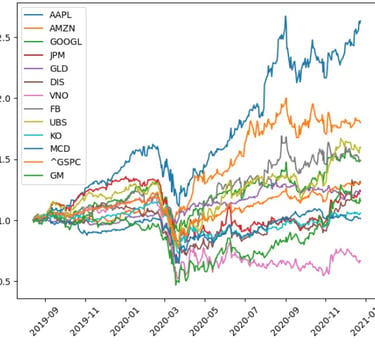

This project provides a comprehensive overview of stochastic modeling for financial assets. The notebook begins by importing essential Python libraries for data manipulation and visualization, such as pandas, numpy, and matplotlib. It then demonstrates how to retrieve and preprocess financial data for a given stock ticker, in this case, SPY, from a CSV file. The core of the project involves defining and simulating three different stochastic models. First, a simple Brownian Motion model is presented. This is followed by a Geometric Brownian Motion model, which is used to generate 2,500 different possible price paths for the asset over 21 periods. Finally, the notebook introduces a Jump-Diffusion Model, which accounts for sudden, large changes in price, and simulates asset price paths using this model as well. The results of each simulation are visualized through plots, illustrating the different behavior and characteristics of each stochastic process.

This project introduces stochastic modeling, demonstrating the simulation of asset prices using Brownian motion, Geometric Brownian Motion, and a Jump-Diffusion Model.